By the time that the agreement had been sent to the Tithe Commission a considerable number of complex tasks had been achieved:

- The Tithe owners had been identified

- The landowners had been identified

- The average value of the tithe paid in the seven years before Christmas 1835 had been calculated

- the area of the parish had been estimated

- the titheable lands had been identified and their areas estimated

- the tithe free lands had been identified

- the moduses had been identified

- an agreement between the land and tithe owners had been agreed.

In the sequence of clauses of the act it was at this point that the appointment of valuers, or apportioners, the terms can be used interchangeably, were appointed, although it is clear that most of the above could not have been completed without the help of a professional valuer. Therefore although strictly speaking some of these tasks belong to the agreement, discussion of them is included here, as a part of the valuer’s role.

Whalley [1] noted that it was in theory “not absolutely necessary to appoint a professional valuer at all.” The landowners could appoint any one of their number to be the valuer “and the person or persons so appointed may make the necessary declaration as valuers, and prepare a draft of the apportionment to be transmitted to the commissioners.” How common this practice was is not known but the act itself demanded that be they amateur or professional, a valuer of some sort had to be appointed for they were “the only persons from whom the commissioners can, under the act, receive the draft of the apportionment, and it is by them that the expenses, great or small, of the apportionment must be in the first instance distributed.”

In order to keep the cost of the commutation to a minimum the ideal number of valuers was one. However clause 32 notes that “in case the majority in respect of number and the majority in respect of interest shall not agree upon the appointment” [of a valuer], “then they shall appoint two or such other even number of valuers as shall be then agreed on.”

Martin worked with other valuers at Corfe, Sydling St Nicholas, Dewlish and Symondsbury in Dorset and at Hartington Mandeville, Merriott, Penselwood and Somerton in Somerset. The relatively high percentage of double valuers in the Somerset commutations suggest there was more distrust of valuers from outside of the county. In three out of the four Somerset parishes which Martin commuted, the Earl of Ilchester was a major landowner and he may have insisted on Martin’s appointment to protect his own interest. Alternatively perhaps the other owners saw Martin as being the Earls man and simply wanted a counterweight to him to ensure fairness. At Dewlish and Sydling St Nicholas he worked with John Baverstock Knight and with John Symonds at Symondsbury.

Unusually at Merriott and Somerton three valuers were appointed which was[in theory at least] not allowed under the act. Where an even number of valuers were appointed they had to nominate an umpire before the apportionment began, who had the final say in case of any dispute between the valuers and it is possible that one of these was an umpire. The appointment of an umpire was not an uncommon practice and Martin himself acted as an umpire on several occasions.

The Act did not specify that the landowners advertise for a valuer or apportioner and although some parishes did so, it was not common and I have found no adverts from any of the parishes he was involved. Very occasionally the parish would advertise the valuers name, as at Silverton in Devon in November 1837; “A meeting of the landowners or their agents was held last week at Silverton, in this county, for the purpose of appointing persons as valuers and apportioners of the tithes of that parish under the new Commutation Act,- when Mr John Drew, of St Thomas and Mr Martin of Evershot, Dorset were elected.- In addition to the duties already stated they will have to measure and map the parish.” In the event John Drew alone undertook the apportionment. We do not know why Martin dropped out but failure to proceed at Silverton meant that he has no Devon commutations to his name. There is one entry in the 1838 diary from April where he mentions tendering for a contract,

|

19th April 1838 |

Went to Beaminster to see Mr Russell respg the partition Deed between Mr Cowdry and Mr Petty But he was from home – Saw Mr P Cox & informed him of the Meeting at M Newton to hear objections to Rent charges- Delivered Tender for Corscombe at 1s per acre and to be found a Man |

Similarly there is only one entry where he attended a meeting where he was appointed the valuer.

|

16th November 1838 |

Attending the Chelborough Tithe Meeting when I was appointed the apportioner and dined at Mr Crew Jennings’s |

In the case of a voluntary agreement the appointment of the valuer was entirely at the discretion, and expense, of the landowners. Whalley notes that it was usual for “landowners to make a separate contract for the preparation of a map; this map however when made, the valuers are not bound to adopt.” In fact it must have been much more convenient to appoint a valuer who would also make a survey and produce a map and with the exception of Somerton and Oborne it seems that Martin also made the maps in parishes where he was also a valuer.

After appointment the valuer had to make an oath before an assistant tithe commissioner or justice of the peace and we can imagine Martin taking it:

“I, John Martin, of Evershot, do solemnly declare, that I will faithfully, impartially and honestly, according to the best of my skill and judgment, fulfil all the powers and duties of a valuer or umpire, under an act passed in the 6th and seventh year of the reign of King William the fourth, intituled, “An Act for the commutation of tithes in England and Wales.””

The oath does not appear in the instrument of apportionment.

Most of this was fairly standard practice, the list of owners and occupiers was no more than a book of particulars and the land measurement and mapping no more than an estate survey. There were though a number of bells and whistles to add to the interest.

Modo decimandi.

The tithe rent charge that had been agreed was made up of three components [2]. The first was the value of any tithe paid in kind, the second were any monetary compositions in lieu of the tithe in kind and finally there were moduses. They are mentioned here as they are of some interest although their elucidation took place and their value included in the rent-charge before the agreement was signed.

By the 19th century payment of the tithe ‘in kind’, that is in real, milk or hay or wheat or lambs etc., had been drastically reduced in its extent. When historical interest in the tithe was at its peak, in the 1970’s and 80’s, there was considerable discussion as to what extent it had persisted. In the commutations in which Martin was involved, only two parishes specifically mention tithing in kind. The entries for both Manston and Winterbourne Monkton are exactly the same, “Whereas I find that all the Lands of the said Parish are subject to payment of all manner of Tithes in kind” but it is likely that in many parishes some part of the tithe was paid in kind.

Over the centuries it became less and less convenient to pay the tithe in kind and a number of alternatives were introduced; sometimes more land was given in lieu of the tithe, sometimes a monetary payment known as a composition was agreed between the rector and the landowners. There was one alternative to the tithe which was the cause of great controversy. This was known as a ‘de modo decimandi’ or, as it was usually known, a modus.

Considerable angst was created by tithing milk in kind. Without any form of refrigeration milk had a short usable life span and unless the rector had the ability to turn it quickly into butter or cheese much must have gone to waste. Another problem arose as to what a tenth meant in the context of milk. Did it mean a tenth of the daily milk should be given or the whole of the milk every tenth day? Then again cows were often milked in the fields and then the question arose as to whether the milk was to be delivered to the rectory or left in a pail in the field for the rector to collect? The answer in parishes without a modus appears to have depended on how the farmer and priest got on.

Since the injunction to pay the tithe was a divine [Canon] law it was left to the Archbishop of Canterbury, Robert Winchelsey to find an answer to the problem. The year was 1305. His answer was to substitute a monetary payment in lieu of the milk and this is the first historical reference to a modus. Such was the Archbishops confidence in the future that he never imagined that the value of the modus would diminish but of course over the centuries the monetary value of the modus declined. It was also extended to a whole range of other agricultural products as we will see.

By the early 1800’s the value of the modus in relation to the value of the tithe it replaced was much, much less. The failure of moduses to maintain their true value meant that they were loved by the farmers and hated by the church for they had the effect of reducing the value of what had been the tithe to well below its notional tenth part. They were one of the principle if not the principle causes of litigation in the early 19th century when the church attempted to overturn many of them. [In depth : Modo Decimandi ]

Another term that occasionally appears in the tithe apportionments is, ‘de non decimando’. This was where the land or parts of the land of a parish or manor were completely exempt from paying tithe. The exemption was said to be by ‘prescription’ and there were several forms.

The most ancient was to give an area of land to the rector, the income of which matched the tithe it was to replace. This was known as a ‘real’ composition. [3] By the 19th century the practice had died out although a modified form of real composition took place at the time of inclosure. Many parishes got rid of the tithe completely at inclosure but it was not universal.

The second form of exemption came about following the dissolution of the monasteries. This created a new level of complexity. Some two thirds of the land went to the new, Henrician Church. The main beneficiaries were the Bishops and much of the land was used to provide income to support the wages of the clerical offices of the cathedral. Had the occupants of these offices [the prepends] farmed the land directly no tithe would have been due but as few if any had an interest or the time for farming they leased the land instead to tenant farmers who in addition to their rent now had to pay tithe. The practical difficulties of collecting tithes from distant parishes, particularly when paid in kind, meant that the prebendaries frequently leased the collection of tithes to others.

About a third of the land was purchased by lay men who, being secular, should, by rights, have paid tithe on the land that they acquired. Contrary to popular belief most of this land was sold at market value and, perhaps to sweeten the deal, Henry VIII passed a statute in 1540 enacting that all who bought monastic lands should hold it tithe free so long as they were in possession and farmed the land themselves. If they had tenants then the tithe had to be paid.

Rent-charge.

When the apportionment of a parish had been completed the valuer produced an “Instrument of Apportionment” which was sent to the Tithe Commission for their confirmatory seal. We will look at an Instrument in detail later but suffice it to say that the first part of the Instrument is a re-iteration of the agreement or award following which there is a page which sits alone and rather oddly within the instrument.

In some later apportionments, for reasons that will be described, it is missing entirely but it was, for the rector at least, the most important part of the apportionment. There were two reasons for this. The original, espoused, purpose of the tithe, paid in kind, was to support the church and it’s priests and to give alms to the poor. By the 19th century payment in kind had almost disappeared, the repair of the church had passed to the parishioners [with the exception of the chancel] and alms giving had by and large ceased. The rent-charge could be seen as little more than the priests salary paid by the farmers. It was hardly in the spirit of the tithe. However the rent-charge was linked to the price of corn and no doubt the clergy consoled themselves with the thought that it maintained the historic link with agricultural produce.

The rent-charge was based on an old method for setting rents which linked them to the price of corn [4] the idea being that as the price of corn went up or down so did the rent. Known as corn rents we see Martin involved in preparing a table [diagram] of corn prices for just such a purpose.

|

5th April 1827 |

Doing a Job for Mr Wm Jennings Diagram of the Prices of Corn |

This rather odd page represents the link between the historic tithe and the rent-charge. It always took the same form.

|

“NOW I John Martin of Evershot in the County of Dorset having been duly appointed VALUER to apportion the Total Sum agreed to be paid by way of Rent-Charge in lieu of Tithes, amongst the several Lands of the said Parish of Child Okeford Do HEREBY apportion the Rent-charge as follows:- GROSS RENT-CHARGE payable to the Tithe-owner in lieu of Tithes for the Parish of Child Okeford in the County of Dorset Two Hundred and Seventy Pounds [5] Value in Imperial Bushels and Decimal Parts of an Imperial Bushel of Wheat, Barley and Oats”

|

At first sight it is difficult to know what this means but the devil is as ever in the detail. Martin has divided the rent-charge into three amounts of £90. He has then asked the question; “For each of these three grains, how much of them could be bought for £90 at the price prevailing as of Christmas 1835?”

Before showing how it was done a simplified example follows for one grain only and in modern money. Suppose the rent-charge is settled at £100 and the price of corn is 50p per bushel [6] the question was then asked “how many bushels of corn can be bought with the awarded rent-charge?” The answer of course is 100 × 0.5 = 200 bushels.

It was this figure, not the amount of rent-charge itself, that was the most important part of the whole commutation for the rector as it determined, each year, how much actual money the Rector was paid.

Suppose that the next year the price of corn was £1 a bushel; the question now asked was not how much wheat can I buy with £100 BUT “how much rent-charge is needed to buy 200 bushels of wheat? The answer is of course 200 × £1 = £200 and it was this figure that was paid by the landowners to the rector in that year. Of course if the price of wheat dropped to 25p a bushel then the amount of money needed to buy 200 bushels was 200 × 0.25 = £50 and this was the rectors due.

In practice variations as dramatic as this were avoided by averaging the price of corn for the seven years preceding the year coming and variations were further reduced by calculating across the three grains. Note that it did not actually matter if the parish grew the crop concerned or not. The corn price was simply a benchmark, a reflection of the state of the countries agriculture, against which the rent-charge could be adjusted. We can now see how Martin converted the rent-charge to bushels of wheat etc:

| Corn | Average Price per Bushel of grain over the seven years prior to

Christmas 1835 |

Calculation

The awarded rent-charge was £250 + £20 for the glebe =£270. This is divided between three grains that is £90 per grain. |

Bushels and Decimal Parts |

| s d | |||

| WHEAT | 7 0 1/4 | One pound is 240 pence is 960 farthings.

Seven shillings is 84 pence is 336 farthings + another farthing is 337 farthings. One pound ∴ buys 960 ÷337 = 2.84686 bushels of wheat. £90 buys 90× 2.84686 = 256.37982 bushels of wheat. |

256.37982 |

| BARLEY | 3 11 ½ | One pound is 240 pence is 480 half pennies.

Three shillings and eleven pence is 94 halfpence +1 is 95 half pence. One pound ∴ buys 480÷95 = 5.05263 bushels of barley. £90 buys 90×5.05263 = 454.73684 bushels of barley. |

454.73684 |

| OATS | 2 9 | One pound is 240 pence

two shillings and ninepence is 33 pence. One pound ∴ buys 240÷33 =7.27272727 bushels. £90 buys 90×7.27272727= 654.54545 bushels of oats |

654.54545 |

Almost straight away there was a problem when it was discovered that the average price of wheat as published at Christmas 1835 -7s 11/4 d per bushel had been wrong and the very early commutations had to be corrected to the final value of 7 0 1/4d, seen in this example, at a later date.

For the valuer calculations such as these must have been arduous, involving as they did long multiplication and division. No doubt logarithm tables helped but even so it was a complicated affair and eventually to prove completely pointless.

At first tables were used to convert rent-charge into bushels. One example is “Tithe Commutation Tables showing at one view the Value, in corn-rent of the rent-charge payable in lieu of tithe and its relative value for the year 1837 and under every future variation in the price of corn and Practical digest of the Tithe Commutation Act with explanatory notes and the forms and plans settled by the commissioners”. It’s author W Palgrave Simpson certainly knew how to give a book a title.

Whether Martin had a copy of this is not known but something similar must surely have been on his desk as almost any amount of the awarded rent-charge could be converted into the equivalent number of bushels, at a glance. If the problems of the land surveyor were solved by such a device, what of the rectors and lay impropriators after all going forward it was they who had to recalculate the new rent-charge each year? They had their own problems for each year the price of corn could vary.

In January each year “the comptroller of corn returns for the time being… shall cause an advertisement to be inserted in the London Gazette, stating what has been, during seven years ending on the Thursday next before Christmas-day then next preceding, the average price of an imperial bushel of British wheat, barley, and oats, computed from the weekly averages of the corn returns.”

This is from 1843 [7] and how we might wonder was Charles Edward North to work out the new rent-charge? All he had to do was multiply, in the case of wheat the number of bushels 256.37982 by 7s 7 ½ d. I’m sure you have already guessed the answer!

This is from 1843 [7] and how we might wonder was Charles Edward North to work out the new rent-charge? All he had to do was multiply, in the case of wheat the number of bushels 256.37982 by 7s 7 ½ d. I’m sure you have already guessed the answer!

Eventually they realised that none of this was necessary. Each year a handy little book published by Henry Pyne, rendered these calculations obsolete. It by-passed entirely the question of “how much money is needed to buy xxx bushels of corn?” It simply inflated the original tithe rent-charge each year by a percentage which reflected the percentage change in corn prices over the previous seven years. I won’t begin to consider the complicated equation that underlay the tables but working from 3d upwards any value of the original rent-charge could be converted to the equivalent to be paid for that year.

Pyne’s Value of the Tithe Rent-charge gave revised values for the rent-charge each year.

Pyne’s Value of the Tithe Rent-charge gave revised values for the rent-charge each year.

If the apportioned rent-charge had originally been £25 then in 1843, the price of wheat, barley and oats having increased, its revised value was £26 8s 0 ¼ d.

Valuation and Apportionment.

Compared with what was to come, working out the agreement and even calculating the amount of wheat etc that could be bought must have seemed a doddle. No doubt the landowners were united when coming to terms with the rector about the total amount of rent-charge to be paid, but it was ‘every man for himself’ when it came to apportioning the rent-charge amongst themselves. As Joseph Bennet an ATC from Tutbury said:

“The difficulties of effecting agreements between the tithe owners and tithe payers are as nothing in comparison with the difficulties of fairly and equitably apportioning the gross sum among the landowners, to the satisfaction of all. The landowners are mostly of one mind while they have the tithe owner to contend with; but when that question is disposed of, they begin to think of their individual interests and are opposed to each other as to the principle upon which the rent charge should be divided.”[8]

The politicians were clearly aware of the difficulties that might arise and to encourage the landowners there was a strict time limit. If after six months of the agreement being confirmed no valuer had been appointed, or if the valuer had not sent an apportionment to the commission, then an assistant tithe commissioner would be empowered to apportion the rent charge. This time limit must have been challenging, particularly in the larger parishes and doubtless the Tithe Commission would not enforce the time limit too strictly as long as they were kept apprised of the progress of the apportionment. None of John Martin’s commutations were achieved in this time [nor I suspect were anyone else’s’] and yet no sanctions seem to have been applied to him.

The first stage of the apportionment was to decide the principles upon which the apportionment was to be made. The landowners themselves were to decide how this was to be done and: “They may select what valuers they please, and what number of valuers; they may give those valuers specific instructions, or leave them to apportion by their own discretion, guided only by the general words of the act.”[9]

In the case of Child Okeford the local agent George Bolls indicates how the landowners had decided to apportion the rent-charge. The one hundred and seventy two acres of arable land were to have £53 15s apportioned to it and so on. The £20 for the glebe was a flat charge on the land whatever it grew and so was not included in the calculation.

|

Acres |

£ s d |

|

|

172 |

Arable |

53.15.0 |

|

982 |

Meadow & Pasture |

184.2.6 |

|

402 |

Down |

8.7.6 |

|

21 |

Coppice |

2.2.0 |

|

248. 7.0 |

||

|

Total |

250.0.0 |

Even this was only a starting point however, for who was to say that all the arable or meadow lands were of equal agricultural or monetary value? The general words of the TCA laid down that “if no principles shall be then agreed upon for the guidance of the valuer or valuers,” then the valuer was to divide the rent-charge” having regard to the average titheable produce and productive quality of the lands.”

How widely the ideal of apportioning the tithe rent-charge according to this principle was ever actually achieved has not been studied widely. If we take rental value to be some indication of the quality of the land, and thus productive ability, then Baker [nee Gambier] [10] found that, across Dorset as a whole there was a generally positively relationship between the actual rent paid and the level of rent-charge. This is based of course on the assumption that highly productive lands generated a higher income for the tenant, a higher rent for the landowner and more titheable produce for the tithe-owner. This may or may not have been the case for as she says “there is no direct method of measuring agricultural production before 1866”.[11]

What we are in a position to say is that even though Bolls had agreed that certain totals of the rent-charge should be apportioned to arable, grasslands, down and coppice within those general categories some account was made by Martin of the quality of the land. Taking meadow land as an example and reducing the areas to perches and the rent-charge to pence it is possible to show that the amount of rent-charge apportioned to a perch of meadow land varied from one part of the parish to another.

| Field Name | Acre | Rood | Perch | Rent-charge pence | Rent-charge per perch

pence |

| Higher Ridgeway | 2 | 3 | 35 | 84 | 5.6 |

| Louseland | 3 | 3 | 28 | 196 | 2.75 |

| Blackmoor | 2 | 3 | 11 | 123 | 3.6 |

| Southfield | 1 | 1 | 20 | 72 | 3.05 |

| Ridgeway | 2 | 3 | 18 | 75 | 6.1 |

| Nine Acres | 8 | 19 | 448 | 2.9 |

On the whole the average comes out at about 3d /perch or 40 shillings an acre considerably more than the 25 shillings that Bolls had valued it at. In determining the value of lands other factors were also at play; Gambier gives an interesting example at Godmanstone where the rent-charge was much higher than in neighbouring parishes. The Rector had a secret weapon, for he “not only possessed the right of feeding a specified number of Cattle where he pleased on certain Lands in the Parish, but he also claimed the right of driving them at any time over other Lands whether those Lands were in Tillage or not. It was not therefore the value of the feeding the Cattle, but the annoying right of spoiling Crops &c which induced Mr Bridge to agree with the tithe-owner for the Right Tithes &c at so high a Rental in order that his tenants might be unmolested.”[12] At Newport in Pembrokeshire Pearson and Collier [13] found that the rent-charge increased across the parish from west to east as the town of Newport was approached, they speculated that the rent-charge might have been determined by the distance of fields from the labour supply and market provided by Newport although they admitted this was speculative.

In one commutation, East Chelborough, the apportionment seems to have been based not on the value of land but on the assessment of the landowner to the poor rate: uniquely Martin lists the landowners and the poor rate they paid and the ratio of poor rate to rent-charge is about 4.3: 1 with minor variations.

Pearson and Collier have the final word on the principles of apportionment. Of the surveyor at Newport, Henry Phelps Goode, they had this to say, and it seems to apply equally to Martin, “the tithe surveyor and valuer, was conscious of the variable quality of the land and concerned that this be reflected in the global tithe rent-charge. We can only assume that similar sensitivity is shown in his apportionment of the tithe rent-charge on a field-by-field basis. We must accept, however, that any analysis of the state of cultivation and the productivity of the land as indicated by the tithe rent-charge must ultimately rest on this assumption.”

Initially the landowners were allowed to apportion their part of the rent-charge either field by field or across the whole of their holdings. If the tithe-owners agreed they could apply the rent-charge to certain parts of their estates whilst leaving other parts free. If they adopted a field by field approach they could request that fields traditionally covered by a modus remained subject to a low rent-charge even though other fields in their possession would be charged more. Land that was tithe free originally could be protected from the rent-charge by apportioning onto the other fields or it could be brought into the rent-charge reducing the amount other parts of their land would have paid. It all depended on what was best for the landowner.

If the apportionment were simple then no great difficulties in the apportionment arose. At Melbury Sampford for example the one thousand and twenty four acres of the parish, paid a rent-rent charge of fifty seven pounds. There was only one landowner -the Earl of Ilchester however and it probably mattered little to him how the apportionment was made. In the event he decided to apportion it on to his gross estate rather than individual fields-which doubtless reduced the costs he had to pay since less work in valuing was required.

At Fordington [14] on the other hand the challenge must have been considerable. Martin had to distribute a fixed amount of money amongst the two thousand two hundred and twelve strips of land [15] of varying size belonging to ninety land owners including Dorchester Council, its burial board, the Overseers of the Poor, the government, the Prince of Wales, the Earl of Ilchester, one public school, various prebendaries of Salisbury and one General in the army. There were three rectors each with different claims, some of the land was tithe free and that which wasn’t had a modus for milk across the parish. This was sudoko on a massive scale.

Apportionment- the practice

Having agreed the principle’s of apportionment the valuer set to work and the amount of rent-charge to be distributed the valuer set to work. Two things remained to be done, firstly the construction of a map, which we will discuss in another section and secondly the written details of how the rent-charge was to be apportioned. Following his time in the field he prepared his draft apportionment. This always followed a standard layout. Firstly came the ‘Landowners’ defined for the purpose of the act as anybody who was in legal possession of the land or its rents and profits. Naturally this included freeholders but others who held the land on customary tenures such as copyholders or life-holders [16] were also considered landowners. Landowners were a mixed bunch.

At Child Okeford there were forty five different landowners over half of whom owned less than 20 acres. As the land belonged to them they were nominally at least the people to pay the rent-charge although, as in the past, there is good evidence that the occupiers paid and deducted the same from the landowner rent. Next come the occupiers, some thirty four of them who lived in the ‘dwelling-houses’ [always specified in this manner], worked the land or who just lived in the cottages..

This simple picture is complicated however for there were any number of arrangements. Sometimes the landowner had the land ‘in hand’, living or farming the land themselves. Sometimes the land was occupied by tenant farmers who themselves were land owners, or by tenants without any land.

The apportionment is laid out in alphabetical order although in some transcriptions [those from Ancestry for example] the layout is in numerical order according to the plot number.

Whalley gives several ‘worked’ examples of how to complete the apportionment. In practice the vast majority were hand written.

The name of the parcel of land, its area in acres roods and perches and its state of cultivation is recorded if the rent-charge was to be apportioned field by field the next column gives the amount of tithe to be apportioned to the parcel divided between the rector and the vicar [if there was one] or the lay impropriator.

Neither the instrument of commutation or the draft apportionment were small. The instrument was written on parchment 18 ¾ inches wide and 21 1/3 inches deep and at Child Okeford amounted to twenty six sheets: Kain found the longest apportionment document nationally to be three hundred and ninety nine sheets long. The draft apportionment was written on paper and had to be signed and sent, together with the map, by the valuer to the tithe commissioners. He had also to send copies of the minutes of the meeting at which he [they] were appointed and also the signed copy of the oath that he had taken. The commissioner had also to “cause a copy of the same to be deposited at some convenient place within the said parish for the inspection of all persons interested in the said lands or tithes”.

After the deposition of the copy draft apportionment a meeting was held to hear objections. Section 61 of the act stipulated that “some assistant commissioner at such meeting as aforesaid shall hear and determine any objections which may be then and there made to the said intended apportionment”. Whalley pointed out that the terms of the act required an ATC to attend such a meeting even when there were no objections – he regarded this as a waste of money. “The valuer, or the person by whom the apportionment is made, will of course be the defendant in this appeal; he will have to justify his apportionment” this cannot have been pleasant for the valuer but presumably they got used to it. The other landowners may not have been so happy however as “It has already appeared from experience, that parties who mean to appeal on the ground, that the sums assessed to other landowners are too low, as compared with their own assessment”.

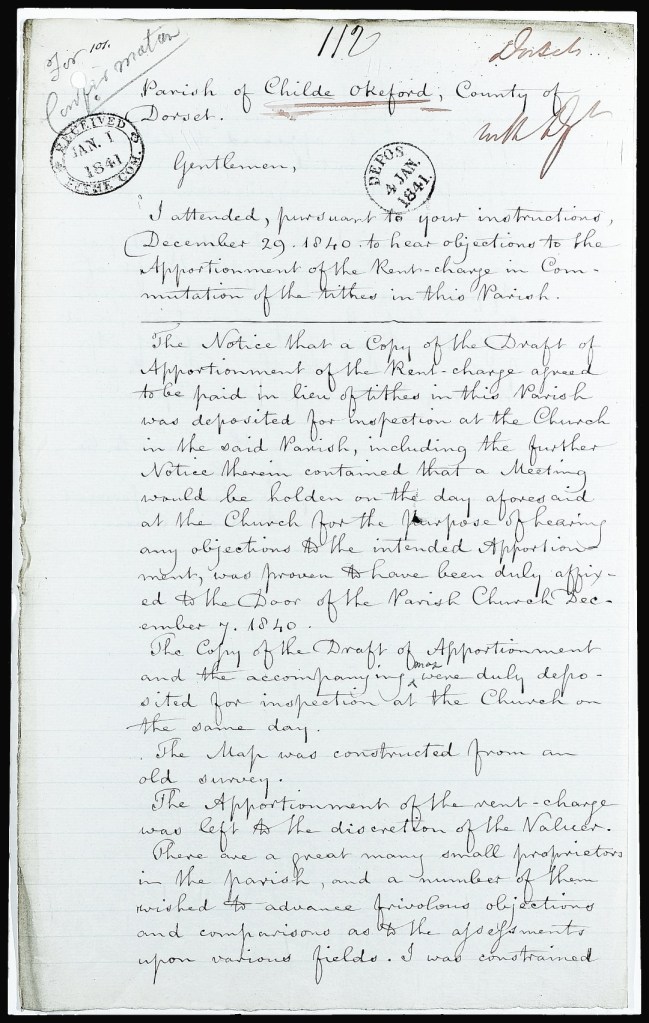

In December 1840 Aneurin Owen, one of the ATC’s received instructions from the Tithe Commission to attend a meeting in Child Okeford at which objections were to be heard.

Letter from Aneurin Owen ATC to the Tithe Commission detailing the events at the meeting held to hear objections at Child Okeford. Jan 1841. Photographed for the author by National Archives.

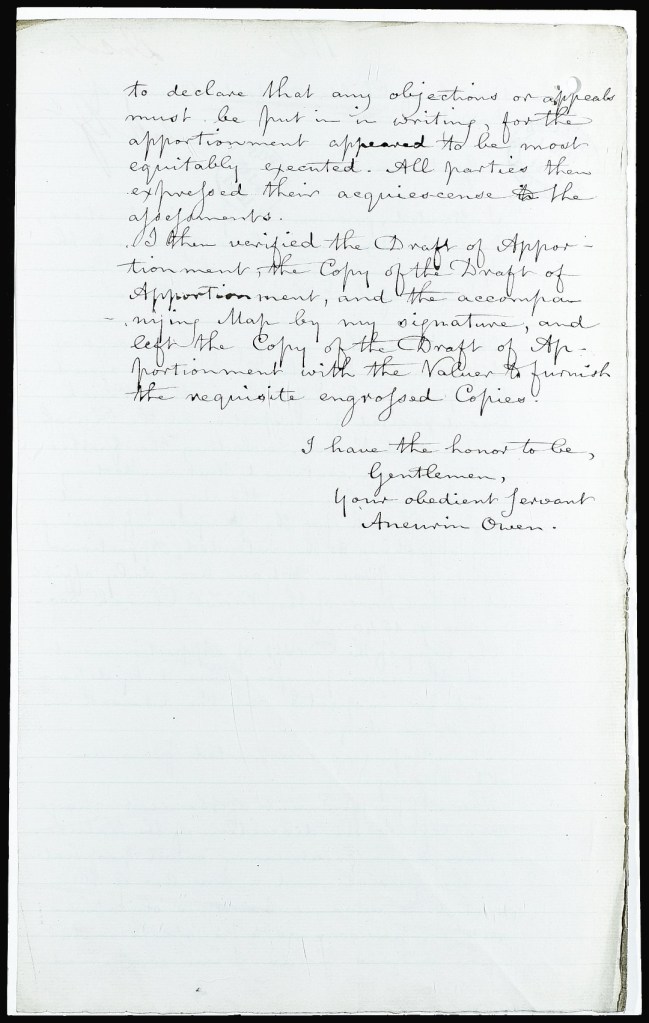

Owen notes once again the presence of a pre-existing map from which the tithe map had been ‘constructed’ and his comment “There a great many small proprietors, in the parish and a number of them wished to advance frivolous objections and comparisons as to the assessments upon various fields” must have been reported countless times in any number of parishes as may the reason that he had to reject their objections:“I was constrained to declare that any objections or appeals must be put in writing”. In the event he exonerated Martin: “for the apportionment appeared to be most equitably executed. All parties then expressed their acquiescence with the assessments.”

| Parish of Childe Okeford, County of Dorset

I attended, pursuant to your instructions December 29 1840 to hear objections to the Apportionment of the Rent-charge in Commutation of the tithes in this Parish. The Notice that a Copy of the Draft of Apportionment of the Rent-charge agreed to be paid in lieu of tithes n this Parish was deposited for inspection at the Church in the said Parish, including the further Notice therein contained that a Meeting would be holden on the day aforesaid at the Church for the purpose of hearing any objections to the intended Apportionment was proven to have been duly affixed to the Door of the Parish Church December 7 1840. The Copy of the Draft of Apportionment and the accompanying ^ Map were duly deposited for inspection at the Church on the same day. The Map was constructed from an old survey. The Apportionment of the rent-charge was left to the discretion of the Valuer. There a great many small proprietors, in the parish and a number of them wished to advance frivolous objections and comparisons as to the assessments upon various fields. I was constrained to declare that any objections or appeals must be put in writing, for the apportionment appeared to be most equitably executed. All parties then expressed their acquiescence with the assessments. I then verified the Draft of Apportionment, the Copy of the Draft of Apportionment and the accompanying Map by my signature, and left the Copy of the Draft of Apportionment with the Valuer to furnish the requisite engrossed Copies. I have the honor to be, Gentleman, Your obedient Servant Aneurin Owen. |

With the ATC’s report in their possession the Tithe Commission would consider whether it should be confirmed. Sometimes outstanding queries remained to be resolved before final confirmation could be given. An example of this is seen at Sydling St Nicholas where three queries were returned to Martin to solve. The parish was a large one of over five thousand acres, four hundred and thirty one plots and some eighty two occupiers. It was unusual however in that the apportionment was made on groups of closes rather than individual fields. This made life slightly easier for the Commission for one of the checks was to ensure that the sums literally added up. A single addition error occurred on page 13 of the apportionment was noted and he had to correct it. A further transcription error was also noted between one of the pages of the apportionment and the summary page. When you consider that there were over fourteen thousand tithe districts in England and Wales and every page of every apportionment had to be checked – all without the use of a calculator. A considerable achievement indeed. When all was agreed the Commissioners would sign and seal the apportionment and map.

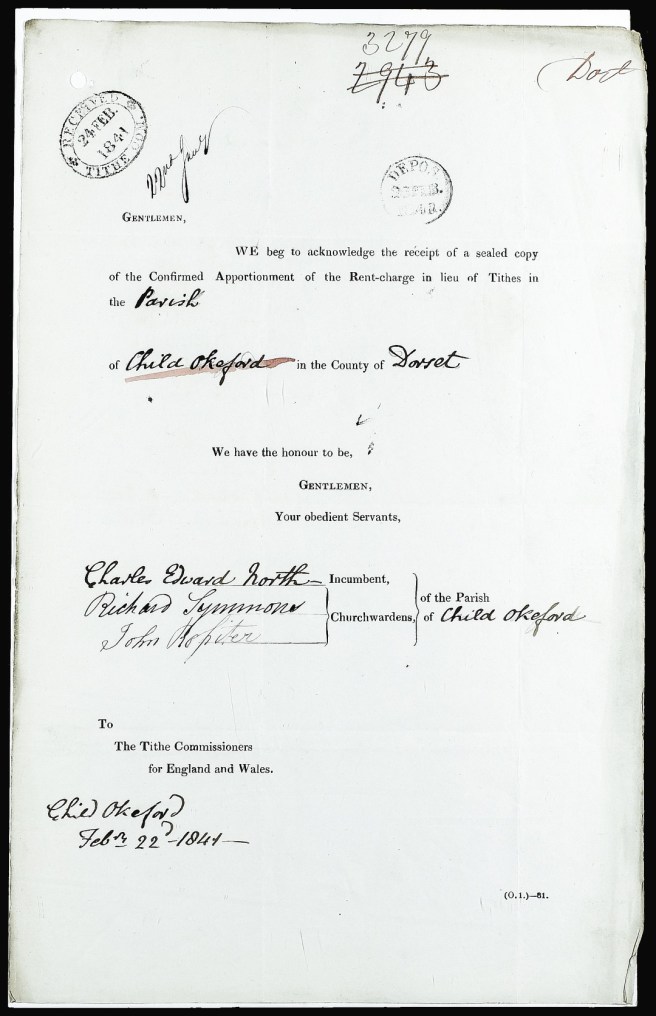

Once the final instrument was confirmed two further copies were made and sent to the rector of the parish and to the registrar of the diocese. These copies were not always made by the valuer or surveyor but it is my belief that John Martin made all the copies of his maps.

Two receipts for sealed copies of the confirmed apportionment. That on the left has been signed by the rector, Charles Edward North and the Church Wardens Richard Symmonds and John Rossiter, both tenant farmers in the parish. The other is from Edward Davies Registrar of the diocese of Salisbury.

Next The Instrument of Apportionment

Previous An Inspector Calls

1 Whalley G H The Tithe Act and the Whole of the Tithe Amendment Acts 2nd edition 1848

2 The value bing averaged over the seven years before Christmas 1835.

3 Real property is land and buildings; personal property is things like money, jewellery and so on.

4 Corn in this sense means wheat. Corn today means maize, which although known to the Europeans, appears not to have been widely grown at this time.

5 £250 plus £20 for the Glebe.

6 One Bushel = 8 gallons=36.4 litres.

7 The Value of the Tithe Rent-charges for the year 1843 by Henry Pyne Published by Authority of the Tithe Commissioners

8 Quoted in Eric Evans Tithes and the Tithe Commutation Act

9 Whalley ibid

10 Tithe Rent-charge and Agricultural Production in mid-nineteenth century England and Wales Baker 1993 BAHR vol 41 169-175

11 Baker ibid

12 Baker ibid

13 The Integration and Analysis of Historical and Environmental Data using a Geographical Information System:

Landownership and Agricultural Productivity in Pembrokeshire c 18 50 BAHR vol 46 p162-176

14 Now a suburb of Dorchester but then a separate village.

15 It was still farmed under the common [open] field system.

16 By which I mean leaseholders who held the land according to a number of lives rather than short term leaseholders holding land for a short number of years.